People continued to use less cash last year with new figures showing the number of withdrawals from ATMs fell 6 per cent annually.

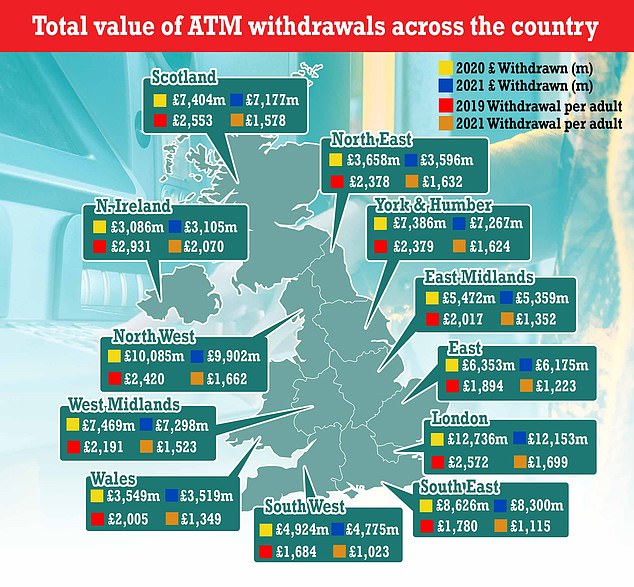

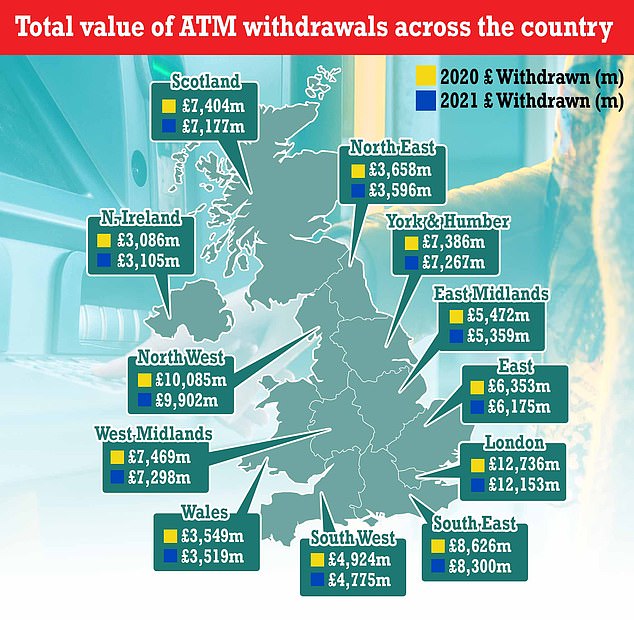

A total of £79billion was withdrawn from cash machines in 2021 compared to £81billion in 2020, according to data by Link, the UK’s main cash machine network.

There was also a 7 per cent decline in cash machine transactions last year, which includes withdrawals and balance enquiries, falling from just over 1.6billion to 1.5billion.

Cash hotspots: Those in Northern Ireland withdrew £2,070 on average last year compared to £1,023 in the South West

This means the average withdrawal per person in the UK was £1,462 last year, visiting an ATM around 18 times.

In 2019, prior to the pandemic, the average withdrawal per person in the UK was £2,193 meaning the typical person is withdrawing two thirds of what they were before Covid-19, when the advice was to not use cash but contactless debit and credit card payments instead,

Andrew Hagger, founder of MoneyComms, believes usage will never return to pre-pandemic levels.

‘I can’t see the number of ATM withdrawals returning to pre-covid levels,’ he said, ‘there has been a real shift towards card instead of cash as the preferred form of payment for retailers and consumers.

‘I don’t think it will snowball from here, but I would expect to see a gradual decline in ATM cash withdrawals annually as people become accustomed to card payment being the norm.’

Although the pandemic has sped up the transition away from cash, the previous years had seen declining use.

The average British banking customer withdrew £1,462 from cash machines in 2021.

People have increasingly been using alternative methods such as contactless cards as well as shopping online.

Before the pandemic, ATM transactions were typically declining 10 per cent annually, according to Link.

Following the successive lockdowns and government restrictions, 2020 saw a 40 per cent collapse in the number of withdrawals compared to 2019 with the total value withdrawn falling from £116billion in 2019 to £81billion in 2020.

Graham Mott, director of strategy at Link said: ‘This is beginning to feel like the new normal.

‘Locations such as markets or even pubs that pre-pandemic only accepted cash, now all have card readers and continue to actively encourage contactless payments.

‘Therefore, some consumers who are confident using digital or contactless payments, now use cash less often than they did pre-pandemic and seem unlikely to ever revert back.’

Historically, parts of London have been ahead of the curve in adopting alternative payment methods such as contactless cards or mobile payments.

Northern Ireland remains the most cash heavy of the nations with Northern Irish banking customers withdrawing an average £2,070 in 2021 compared to the South West, where the average customer withdrew £1,023.

However, the analysis shows that while some areas of the country have seen a steeper drop in withdrawals, overall, it is a similar picture across the UK.

In 2021 as UK banking customers withdrew £79 billion from cash machines compared to £81 billion in 2020.

As many as five million people are at risk of being left behind as Britain marches towards a cashless society, according to Link.

There is now at least some reason for optimism for those that remain cash reliant despite close to 5,000 bank branches having shut down since 2015.

Last month, a landmark agreement was reached between the major banks to share services to ensure long-term cash availability across the UK.

Under the agreement, any community that faces the closure of a core cash service, such as a bank branch or ATM, will have its needs independently assessed by Link, which will then determine whether a new solution should be provided to meet that community’s cash needs.

New services giving access to cash have already been announced for this year, including the installation of free-to-use ATMs in 11 locations.

The Post Office has announced it will install ‘dedicated cash services’ in 30 branches over the next 12 months which could include banking counters and self-service machines.

Furthermore, five more shared banking hubs will be launched by Easter this year in Acton, West London, Brixham in Devon, Carnoustie in Angus, Knaresborough, North Yorkshire, and Syston in Leicestershire.

There are also other industry initiatives to support cash and banking, such as the ‘cashback without purchase’ scheme enabling people to get money from retailer’ tills without having to buy anything in more than 2,000 UK stores.

These are primarily made up of convenience stores such as the Co-op, Londis, Spar, Nisa and other smaller-scale retailers.

THIS IS MONEY’S FIVE OF THE BEST CURRENT ACCOUNTS

Santander’s 123 Lite Account will pay up to 3% cashback on household bills. There is a £2 monthly fee and you must log in to mobile or online banking regularly, deposit £500 per month and hold two direct debits to qualify.

![]()

Virgin Money’s current account offers a £150 Virgin Experience Days gift card or 12-bottle case of Virgin Wines when you switch and pays 2.02 per cent monthly interest on up to £1,000. To get the bonus, £1,000 must be paid into a linked easy-access account and 2 direct debits transferred over.

Club Lloyds’s Current Account pays 0.6% interest on balances of up to £3,999, while those with sums of between £4,000 and £5,000 will earn 1.5% on that balance. There is no cost if you pay £1,500 each month, otherwise a £3 fee applies. Must hold two direct debits.

First Direct will give newcomers £130 when they switch their account. It also offers a £250 interest-free overdraft. Customers must pay in at least £1,000 within three months of opening the account.

![]()

Nationwide’s FlexDirect account comes with up to £125 cash incentive for new and existing customers. Plus 2% interest on up to £1,500 - the highest interest rate on any current account - if you pay in at least £1,000 each month, plus a fee-free overdraft. Both the latter perks last for a year.

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.